Robert Kiyosaki's book, 'Retire Young Retire Rich' makes a brash statement that it can teach you "How to get rich quickly and stay rich forever!"

This book is all about leveraging. The power of leveraging. Your mind is one of the most powerful form of leverage in the world and what you think and believe will influence how you make your decisions and take action. Laws of attraction.

How to leverage your mind, how to leverage your plans, how to leverage your actions and the leverage from taking that first step.

The three main assets that you can employ to enable you to retire young and retire rich are:

1. Real estate

2. Paper assets/stocks/shares

3. Businesses

Most of his books have repetitious sections and again, constantly spruik his own cash flow game and various other products. For the sake of this book analysis, I read everything.

Leveraging your mind

* Learn investment terminologies and words. The more financial words you learn, the greater your ability to invest and take advantage of various investments

* How did Kiyosaki get wealthy and successful? He writes that it was by increasing his:

a) Business skills

b) Money management skills

c) Investment skills

* Words that will work against you:

a) "But we don't have any money."

b) "I can't do that."

c) "I'll think about it next year, or once Kim and I get settled."

d) "You don't understand our situation."

e) "I need more time."

f) "Maybe someday when I have the money I'll begin to invest."

g) "Do you know how busy I am? I don't have the time to to learn to invest."

If you haven't got any funds to invest, then you can invest in your financial knowledge by taking the time to learn about investing in property, stocks and businesses. It costs nothing to acquire financial knowledge now that you can use the internet and you can always go the old school way and borrow books from the library. It's free to attend auctions, free to ask questions, free to attend open houses and free to analyse investment deals even if you haven't got the funds to invest. By the time you DO have some funds to invest, you will already be an investment pro to some extent because of the time that you've spent investing in your financial knowledge.

* "...the middle class and the poor fall behind the rich is because they use the financial power of bad debt to fall behind in life. The rich use the financial power of good debt to propel them ahead."

* Kiyosaki believes that his wealth resulted from the three asset classes mentioned (real estate, paper assets and business) and these were magnified by leveraging OPM (other people's money) and OPT (other people's time).

* Kiyosaki doesn't believe in someone being lucky simply by being at the right place at the right time. Luck happens only when you're "educated, experienced, ready and prepared to take advantage of the opportunity when the opportunity presented itself".

* The million dollar question that you can ask yourself. If you can answer this question, then you can create your own leverage into wealth: "How can I do what I do for more people with less work and for a better price?"

* "A person who thinks investing is risky will often find all the reality they want to substantiate that reality." Change your reality and your views in life by choosing to say, "How can I afford that piece of beachfront property?" instead of saying,"I can't afford it."

* Three form of income is mentioned:

a) Earned income - from your personal labour, your pay cheque, when you get pay rises, bonuses, overtime and commissions etc

b) Portfolio income - from your stock portfolio such as stocks, bonds, mutual/managed funds

c) Passive income- from real estate, royalties, patents and intellectual properties

* Earned income is disliked by Kiyosaki's 'rich dad' due to various reasons:

1. Highest taxed income with the fewest control over how much tax you pay and when you pay your taxes

2. You have to personally work for it using your valuable time

3. There's very little leverage in earned income and the primary way to increase earned income is by working harder

4. There is often no residual value for your work. If you don't work, you don't get paid.

* Again, Kiyosaki repeats himself from previous books:

a) Employee -> Earns, taxed, spends what is left

b) Business owner -> Earns, spends, pays tax on what is left

I'll use a simple example to illustrate this concept for you:

a) Employee with 30% tax -> Earns $100, is taxed $30, spends $20, is left with $50 in the pocket

b) Business with 30% tax-> Earns $100, spends $20, is taxed 30% on $80, is left with $56 in the pocket

* "The idea of working all your life, saving , and putting money into a retirement account is a very slow plan. It is a good and sensible plan for 90 percent of the people. But it is not a plan for someone who wants to retire young and retire rich. If you want to retire young and retire rich, you need to have a plan that is far faster than the plans of most people."

* "...you need to invest in what is going to happen, rather than what has already happened...If you want to see the future, you need to see it through younger eyes."

* "Over the years, we have attended many investment seminars, seminars on marketing, sales, systems development, handling employees and of course investing...I meet authors who did well in school as writers but their books do not sell as many as mine do. When I suggest to them that they attend direct marketing courses, or sales training courses, or copy writing classes, many get very indignant. As I said in Rich Dad Poor Dad, I am a best-selling author not a best-writing author."

* Calculate your wealth ratio. The goal is to have your passive and portfolio income exceed your total expenses so that even if you quit your 'earned income' job, you can still maintain your lifestyle. Once the ratio is 1 or higher, it's a choice whether you wish to quite the 'rat race' or not:

Wealth Ratio = Passive income + Portfolio income

Total expenses

Example: $600 passive + $200 portfolio = 0.2 wealth ratio

$4000 total expenses

* "When I think of the millions of people who are betting their financial future and their financial security on a stock market I cringe. Millions of people are worried about their financial future as the number of layoffs increase and the market continues to fluctuate....there are stories of how retirees have lost most of their retirement savings to investment advisers and insurance salespeople they trusted..."

* "Your life will change forever once you know the difference between saving money and making money."

* "The most life destroying word of all is the word tomorrow...the poor, the unsuccessful, the unhappy and the unhealthy are the ones who use the word tomorrow the most. These people will often say, 'I'll start investing tomorrow,' or 'I'll start my diet and exercise tomorrow.'"

* If you see an opportunity arise but were unable to take advantage of it, then "you are at the boundaries of your context, what you think is possible for yourself, and your content, which is the accumulated knowledge via which you handle problems and challenges..."

* Kiyosaki spends pages and pages writing about your reality, how people

don't realise that their reality is only limited by their mind. If you

don't expand your reality then you will never see the answers to your

problems because you are trying to solve your current problems with your

existing knowledge and experience: "Most people try and solve their financial problems with what they know, rather than expand what they know so they can solve a bigger problem. Rather than taking on bigger financial challenges, most people wrestle all their lives with financial problems they feel comfortable with."

* In the book, 'Who took my money', you read about the E and S side of the quadrant and the B and I side of the quadrant. The goal is to move to the B-I side of the quadrant because income on the E-S side is limited whereas the earning potential from the B-I side is unlimited: "The trouble with selling your labour is that there is only so much you can do. If you learn to acquire or build assets to generate money, you can slowly but surely increase your income...your labour has no long term residual value. If you buy a rental property and you profitably rent it out, the labour you used to acquire that rental property can be rewarded over and over again, for years."

* "If you work slowly acquiring assets your income potential is infinite and that income can be passed on for generations to come. Your job or profession is not something you can pass on in your will to your children."

* "It is not your boss's job to make you rich. Your boss's job is to pay you for what you do, and it is your job to make yourself rich at home and in your spare time."

* "The moment you sincerely build a business or invest to increase your service to more people, you have forever increased your chances of becoming extremely wealthy and retiring young and retiring rich."

Leverage of habits that will make you rich

1. Hire a bookkeeper - having a bookkeeper keep your income, expenses, assets and liabilities in line so that you can keep professional records, have an unemotionally attached third party review your financial challenges so that you can make corrections via a monthly review of your financial situation

2. Create a winning team- the B+I quadrants are 'team sports' requiring team members such as your banker, accountant, attorney, stockbroker, real estate broker, insurance broker etc

3. Constantly expand your context and your content

4. Keep growing up- doing things differently as we grow older instead of doing the same old thing day in day out.

5. Be willing to fail more- by being willing to try new things and make mistakes

6. Listen to yourself- pay attention to what you are saying to yourself and focus on what you want from life and in your life

* "Kim(his wife) and I did not keep our money in a retirement account in order to retire young. We knew that we had to keep our money working, working hard to acquire more and more assets. Once our money acquired an asset, that money was soon reemployed to go out and get us another asset. The strategy we used to keep our money moving and acquiring more and more assets is a strategy that almost everyone can use."

* Comparing the stock market to the real estate market:

a) The stock market is simply buy or sell

b) The real estate market is negotiable- terms are negotiable, can lower or raise the price, can reduce expenses, can improve the value of the property by renovating such as painting, adding extra bedrooms, selling off extra land etc

* It does not take money to make money - Kiyosaki recommends people engage in option trading. I don't think I fully agree with his recommendation here because although you can write naked call and put options for a minor fee, if the naked options are being exercised by the holders of your put and call options, then you better HAVE the money to be able to buy the stocks off the put option holders or have the funds to buy the shares so that your call option holders can buy the stocks off you. So unless you wish to get into financial difficulty, it DOES take money to make money if you wish to pursue this particular strategy that Kiyosaki is proposing. Anyone trying to pursue this options trading strategy needs to ensure that they have backup funds that can be used to buy stocks off naked put option holders trying to exercise the put option that you sold them and similarly, have the funds to buy stocks that can be resold if holders of naked call options exercise their options.

I have to agree with Kiyosaki with respect to the statement that it doesn't take money to make money. You DON'T have to have money to make money. You can create money in so many ways even if you have zilch. If you are creative or have a great idea, you can sell your ideas. You have talent. You just need to capitalise on your talents, knowledge and abilities. You can create an intellectual property, you can create a blog (like this) from scratch for free and generate advertisement income from Google Adwords and from advertisers wishing to advertise with your blog/website. I created this site from scratch and it didn't cost me a single cent and it's been generating income for me. That's just one example. Obviously the more money you have, the easier it is to buy and create investments and the faster you make more money.

But work with what you've got. If you've got nothing, you can create something from nothing. The sky really is your limit. There is over 6 billion people on this planet and what is stopping you from generating a chunk of revenue from that population?

What would you do if there was no risk and it required no money to become rich?

Kiyosaki challenges us to think about what we would do if there was no risk and no money required to become rich. What type of business or investment or hobby would you start? What trade would you be in? Would you retire? Do you think that type of world exists? If you think that world is non existent, do you think you are destroying yourself by limiting your creativity?

In closing, Kiyosaki writes that "Leverage is power. Leverage is found inside of us, all around us, and invented by us. With each new invention, inventions such as the automobile, airplane, telephone, television, world wide web, a new form of leverage is invented. With each new form of leverage, new millionaires and billionaires are created because they used the leverage, not ruined or abused the new leverage. So always remember that the power of leverage can be used, abused or feared. How you choose to use the power of leverage is up to you and only you."

Tuesday, December 18, 2012

Saturday, December 15, 2012

Robert Kiyosaki: Who Took My Money?

Book review on Robert Kiyosaki: Who Took My Money?

Robert Kiyosaki's book(co-authored with Sharon L. Lechter), 'Who Took My Money?' on "Why slow investors lose and fast money wins" is an interesting read. If you've never heard of Kiyosaki, then you've been living under a rock. He's been on the New York Times Bestseller list multiple times with multiple books.

Although 'Rich Dad Poor Dad' is his most famous book, it's not a favourite of mine. His later books are much better because he becomes a more experienced investor with a better advisory team when he has more money to invest and it's evident in the later books compared to his earlier work. Kiyosaki's book can be annoying to read sometimes because he keeps plugging his own products and boardgame, almost in every single chapter :/

Are Mutual Funds and Managed Funds evil?

Kiyosaki thoroughly dislikes Mutual Funds (for Australian readers, Mutual Funds=Managed Funds, 401(k)=Retirement Funds). He's always denouncing them and telling readers to steer clear of them. I'm not a huge fan of managed funds either. Some are decent (like the index funds with low fees) but the majority has high fees, does not outperform the index (eg All Ords, ASX200) and will charge you fees even if they are losing money hands over fist.

I'm going to highlight the bits that I found interesting or may be of interest to anyone else. 'Who Took My Money'(WTMM) was first published in May 2004, prior to the GFC and mainly reflects on the dotcom sharemarket bust. Ironically, his book is timelessly relevant in light of the GFC crisis that rocked the world in 2008.

WTMM is structured into two sections: "What Should I Invest In?" and "Ask An Investor".

What Should You Invest In?

Kiyosaki doesn't like diversification in simply the stock market. He recommends 'integrating' and using the powers of the following 'financial forces':

1. Business

2. Real estate

3. Paper assets (shares/stocks)

4. Your banker's money (via leveraging/gearing/mortgage loans/margin loans)

5. Tax laws (via depreciation and the ability to deduct expenses prior to paying tax on profits)

6. Corporate laws (via business entity, copyrights, patents etc)

Whereby, the more you can mix and match those particular 'forces', the more you can accelerate your wealth and returns to create 'financial synergy'.

He refers to life as 'The Game of Money' because we work for approximately 40 years. When you're 25-35yo, you're in the first quarter, 35-45 is second quarter, 45-55 is third quarter and 55-65 is the fourth quarter. After 65, you're in overtime and if you're disabled or have some health impediment, then you're 'out of time'.

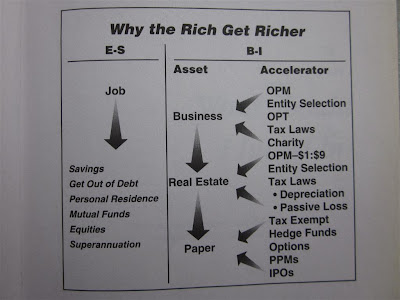

Kiyosaki refers to a cash flow quadrant whereby he recommends moving from the 'employee' and 'self employed' side to the 'business owner' and 'investor' side of the quadrants will accelerate your returns. See below:

Employees and self employed individuals will only earn income whilst their personal labour is involved. If you don't work, you don't earn. Simple. On the business owner and investor side, if you don't work, your business and your investments will still generate passive income for you.

Employees and self employed individuals will only earn income whilst their personal labour is involved. If you don't work, you don't earn. Simple. On the business owner and investor side, if you don't work, your business and your investments will still generate passive income for you.

The reason why B-I are will help you get richer faster is due to reasons such as utilising OPM(other people's money), choice of operating entity, ability to depreciate your assets against your returns (he refers to depreciation as 'phantom income') and the ability to leverage. Just as the financial institutions use leveraging(on bank deposits) to magnify their returns, you can also use leveraging(from bank/mortgage loans) to magnify your own returns. Savers and depositors earn peanuts on their savings.

The most important aspect of the B-I side which I would also like to emphasise is that you can deduct your expenses against your income prior to paying tax as a business owner and investor. Unfortunately for employees, usually you pay tax first prior to being able to deduct your expenses.

Kiyosaki rather dislikes answering the question, "I have $10k, what should I invest in?". It's a difficult and complex question to answer. Firstly, it depends on your own scenario, how old you are, where you're at in life, what existing debts you have already and where you're at in terms of financial knowledge and experience. If you don't know what to do with your $10k, then the best thing you should do is stash it in a high interest savings account. Go read about investing and then you will have a better idea of what to do with it. Otherwise, you will eventually get fleeced.

He writes that simply putting all your savings into a 'mutual fund/managed fund', dollar cost averaging by monthly contributions, crossing your fingers and praying that the stock market goes up is akin to gambling. There are no guarantees that you won't lose money, there are no insurance company that will insure your stock portfolio against losses. You can insure your stock portfolio but you will need to employ put and call options which are techniques that most average and newbie investors are unable to employ.

He contrasts this against buying investment properties. Insurance companies will insure investment properties because it's a more stable investment but they won't insure your stock portfolio. Using these two examples, he illustrates that the stock market IS riskier than the property market.

"One of the reasons so many investors lose so much money is because they pay $10 a month into a fund for forty years and do not know if it will be there forty years from now."

Maybe Kiyosaki was on the foreclosure ball already back in 2004 when he wrote that, "Today in Phoenix, Arizona, the fastest growing major market in America, foreclosures are up. Many people are losing their homes. Investors are bailing out of properites that they paid too much for."

Unfortunately he was wrong thus far on the Australian property market, "In Australia, interest rates are on the rise again, which will mean the greater fools of the property market will be led to slaughter." Property prices have risen significantly since 2004.

Building pipelines

I once read a quote from Napoleon about investing. He said that investing is like planting trees(or was it fruit trees?). It takes many years, but after several decades, you will have a forest to protect and feed you. I like thinking about investing as planting young fruit trees. The more fruit trees planted and the earlier you plant them, the more fruit you will get as they mature over the years and you will beable to enjoy a whole forest and orchard of trees.

Kiyosaki compares investing to building pipelines. Over the years, you wish to expand the diameter of your pipelines. The goal is to "simply build the pipelines and continuously expand the diameter of the pipe" which is a metafore for increasing the amount of passive income and return that flows from your investment. When you first start, it's a drip and over time as you expand your business and or investments, it becomes a heavier flow of passive income.

This post is becoming insanely long so I'll just quote directly from the book without any of my own personal reflections:

* "one of the most important assets an investor needs to manage is their flow of information. One of the reasons many millions of investors lost trillions of dollars is because they received financial information that was of poor quality, late, often biased, and sometimes dishonest."

* "Waiting for the long term...millions of investors, even while losing a lot of money in the stock market, are still waiting for the market and the price of their shares to come back up. That is a waste of time. Although the market will someday be back, the market that they lost their money in is gone...instead of investing for the long term, they are waiting for the long term..."

* "The professional investor follows the following formula:

1. Invest money into an asset

2. Get the original investment money back

3. But keep control of the original asset

4. Move the money into a new asset

5. Get the investment money back

6. Repeat the process ...this process is called the velocity of money...most investors do not realise they too can expand their own money supply and thereby expand their earning power"

* "Consider control and how it differs among the different type of asset classes...

Owning your own business - You are in control

Owning real estate - You are in control

401(k)s /retirement funds - Who is in control?

Mutual funds/managed funds - Who is in control?

Equities/stocks - Who is in control?

... The individual companies have presidents and board of directors who have control over the operation of the underlying business...professional investors want CONTROL over their assets and their cash flow." The ability to control means you can determine how to reduce expenses, how to increase income, when to pay tax (ie when to sell and trigger CGT tax) and your leveraging ability.

* "Many people just turn their money over to total strangers and wonder why they get such poor returns. Or many people seem to think that it should be easy to find a great investment...The fact is, it's easy to find bad investments. The world is filled with people offering you bad investments to invest in. If you want your money to work hard for you, you cannot afford to be lazy."

* "Four green houses...one red hotel...the purpose of business is to make life simpler, not harder. The businesses that make life the easiest are the businesses that make the most money." He employs examples such as cars, phones, supermarket, electric companies etc

* "You should learn to take things that are difficult and make them simple. If you will focus on that, making life easier for people, you will become a very rich person. The more people you help in making life easier, the richer you will become."

* "The power of power investing...it is investing using all three asset classes(business, real estate and paper assets), reinvesting cash flow, leveraged with OPM and accelerated by tax incentives...power investing requires that the investor invest in two, and preferably three, asset classes."

* "...why then do so many more people invest in paper assets and give up so much control? ...the answer...found in the word easy. For millions of people, it is easier to turn over control of their money than to learn how to drive their money. That is why millions of investors have their portfolios filled with mutual funds without any idea of who is driving the fund..."

* Kiyosaki likes paper assets primarily due to their liquidity rather than their long term value. I agree absolutely.

* An employee's cash flow pattern: EARN-->PAY TAX-->THEN SPEND

* A business owner or investor cash flow pattern: EARN-->SPEND--THEN PAY TAX

* "...the five considerations for each investment and how the investment fits into your overall investing strategy:

1. Earn/create- how will it generate cash flow for you?

2. Manage- how will you manage this investment?

3. Leverage- how much leverage will the investment provide, or can you get?

4. Protect- how should you hold the investment, maximise its profitability and protect it from potential creditors?

5. Exit- how will you get your original investment money back?"

That last quote from the book is imo, one of the MOST important part of the investing process. Answering those five points prior to investing will mean you've looked at all the aspects of the cash flow, the potential benefits, protecting your asset and finally, being able to extract your capital so that you can invest in additional assets.

Investing for cash flow is a VERY important concept. If you only invest for capital gains and employ negative gearing as your dominant investment strategy, eventually you will hit a debt servicing capacity wall and be unable to service further investment leveraging due to poor cash flow.

It's been a long time since I've written a book review and now I remember why I don't post book reviews often lol. PHEW!! It has been over two years since I've published material regarding personal finance books. The last one I wrote two years ago, 'Top 10 Books on Wealth' is STILL relevant because they're classic books. You should read that post if you like reading personal financial management books.

Robert Kiyosaki's book(co-authored with Sharon L. Lechter), 'Who Took My Money?' on "Why slow investors lose and fast money wins" is an interesting read. If you've never heard of Kiyosaki, then you've been living under a rock. He's been on the New York Times Bestseller list multiple times with multiple books.

Although 'Rich Dad Poor Dad' is his most famous book, it's not a favourite of mine. His later books are much better because he becomes a more experienced investor with a better advisory team when he has more money to invest and it's evident in the later books compared to his earlier work. Kiyosaki's book can be annoying to read sometimes because he keeps plugging his own products and boardgame, almost in every single chapter :/

Are Mutual Funds and Managed Funds evil?

Kiyosaki thoroughly dislikes Mutual Funds (for Australian readers, Mutual Funds=Managed Funds, 401(k)=Retirement Funds). He's always denouncing them and telling readers to steer clear of them. I'm not a huge fan of managed funds either. Some are decent (like the index funds with low fees) but the majority has high fees, does not outperform the index (eg All Ords, ASX200) and will charge you fees even if they are losing money hands over fist.

I'm going to highlight the bits that I found interesting or may be of interest to anyone else. 'Who Took My Money'(WTMM) was first published in May 2004, prior to the GFC and mainly reflects on the dotcom sharemarket bust. Ironically, his book is timelessly relevant in light of the GFC crisis that rocked the world in 2008.

WTMM is structured into two sections: "What Should I Invest In?" and "Ask An Investor".

What Should You Invest In?

Kiyosaki doesn't like diversification in simply the stock market. He recommends 'integrating' and using the powers of the following 'financial forces':

1. Business

2. Real estate

3. Paper assets (shares/stocks)

4. Your banker's money (via leveraging/gearing/mortgage loans/margin loans)

5. Tax laws (via depreciation and the ability to deduct expenses prior to paying tax on profits)

6. Corporate laws (via business entity, copyrights, patents etc)

Whereby, the more you can mix and match those particular 'forces', the more you can accelerate your wealth and returns to create 'financial synergy'.

He refers to life as 'The Game of Money' because we work for approximately 40 years. When you're 25-35yo, you're in the first quarter, 35-45 is second quarter, 45-55 is third quarter and 55-65 is the fourth quarter. After 65, you're in overtime and if you're disabled or have some health impediment, then you're 'out of time'.

Kiyosaki refers to a cash flow quadrant whereby he recommends moving from the 'employee' and 'self employed' side to the 'business owner' and 'investor' side of the quadrants will accelerate your returns. See below:

The reason why B-I are will help you get richer faster is due to reasons such as utilising OPM(other people's money), choice of operating entity, ability to depreciate your assets against your returns (he refers to depreciation as 'phantom income') and the ability to leverage. Just as the financial institutions use leveraging(on bank deposits) to magnify their returns, you can also use leveraging(from bank/mortgage loans) to magnify your own returns. Savers and depositors earn peanuts on their savings.

The most important aspect of the B-I side which I would also like to emphasise is that you can deduct your expenses against your income prior to paying tax as a business owner and investor. Unfortunately for employees, usually you pay tax first prior to being able to deduct your expenses.

Kiyosaki rather dislikes answering the question, "I have $10k, what should I invest in?". It's a difficult and complex question to answer. Firstly, it depends on your own scenario, how old you are, where you're at in life, what existing debts you have already and where you're at in terms of financial knowledge and experience. If you don't know what to do with your $10k, then the best thing you should do is stash it in a high interest savings account. Go read about investing and then you will have a better idea of what to do with it. Otherwise, you will eventually get fleeced.

He writes that simply putting all your savings into a 'mutual fund/managed fund', dollar cost averaging by monthly contributions, crossing your fingers and praying that the stock market goes up is akin to gambling. There are no guarantees that you won't lose money, there are no insurance company that will insure your stock portfolio against losses. You can insure your stock portfolio but you will need to employ put and call options which are techniques that most average and newbie investors are unable to employ.

He contrasts this against buying investment properties. Insurance companies will insure investment properties because it's a more stable investment but they won't insure your stock portfolio. Using these two examples, he illustrates that the stock market IS riskier than the property market.

"One of the reasons so many investors lose so much money is because they pay $10 a month into a fund for forty years and do not know if it will be there forty years from now."

Maybe Kiyosaki was on the foreclosure ball already back in 2004 when he wrote that, "Today in Phoenix, Arizona, the fastest growing major market in America, foreclosures are up. Many people are losing their homes. Investors are bailing out of properites that they paid too much for."

Unfortunately he was wrong thus far on the Australian property market, "In Australia, interest rates are on the rise again, which will mean the greater fools of the property market will be led to slaughter." Property prices have risen significantly since 2004.

Building pipelines

I once read a quote from Napoleon about investing. He said that investing is like planting trees(or was it fruit trees?). It takes many years, but after several decades, you will have a forest to protect and feed you. I like thinking about investing as planting young fruit trees. The more fruit trees planted and the earlier you plant them, the more fruit you will get as they mature over the years and you will beable to enjoy a whole forest and orchard of trees.

Kiyosaki compares investing to building pipelines. Over the years, you wish to expand the diameter of your pipelines. The goal is to "simply build the pipelines and continuously expand the diameter of the pipe" which is a metafore for increasing the amount of passive income and return that flows from your investment. When you first start, it's a drip and over time as you expand your business and or investments, it becomes a heavier flow of passive income.

This post is becoming insanely long so I'll just quote directly from the book without any of my own personal reflections:

* "one of the most important assets an investor needs to manage is their flow of information. One of the reasons many millions of investors lost trillions of dollars is because they received financial information that was of poor quality, late, often biased, and sometimes dishonest."

* "Waiting for the long term...millions of investors, even while losing a lot of money in the stock market, are still waiting for the market and the price of their shares to come back up. That is a waste of time. Although the market will someday be back, the market that they lost their money in is gone...instead of investing for the long term, they are waiting for the long term..."

* "The professional investor follows the following formula:

1. Invest money into an asset

2. Get the original investment money back

3. But keep control of the original asset

4. Move the money into a new asset

5. Get the investment money back

6. Repeat the process ...this process is called the velocity of money...most investors do not realise they too can expand their own money supply and thereby expand their earning power"

* "Consider control and how it differs among the different type of asset classes...

Owning your own business - You are in control

Owning real estate - You are in control

401(k)s /retirement funds - Who is in control?

Mutual funds/managed funds - Who is in control?

Equities/stocks - Who is in control?

... The individual companies have presidents and board of directors who have control over the operation of the underlying business...professional investors want CONTROL over their assets and their cash flow." The ability to control means you can determine how to reduce expenses, how to increase income, when to pay tax (ie when to sell and trigger CGT tax) and your leveraging ability.

* "Many people just turn their money over to total strangers and wonder why they get such poor returns. Or many people seem to think that it should be easy to find a great investment...The fact is, it's easy to find bad investments. The world is filled with people offering you bad investments to invest in. If you want your money to work hard for you, you cannot afford to be lazy."

* "Four green houses...one red hotel...the purpose of business is to make life simpler, not harder. The businesses that make life the easiest are the businesses that make the most money." He employs examples such as cars, phones, supermarket, electric companies etc

* "You should learn to take things that are difficult and make them simple. If you will focus on that, making life easier for people, you will become a very rich person. The more people you help in making life easier, the richer you will become."

* "The power of power investing...it is investing using all three asset classes(business, real estate and paper assets), reinvesting cash flow, leveraged with OPM and accelerated by tax incentives...power investing requires that the investor invest in two, and preferably three, asset classes."

* "...why then do so many more people invest in paper assets and give up so much control? ...the answer...found in the word easy. For millions of people, it is easier to turn over control of their money than to learn how to drive their money. That is why millions of investors have their portfolios filled with mutual funds without any idea of who is driving the fund..."

* Kiyosaki likes paper assets primarily due to their liquidity rather than their long term value. I agree absolutely.

* An employee's cash flow pattern: EARN-->PAY TAX-->THEN SPEND

* A business owner or investor cash flow pattern: EARN-->SPEND--THEN PAY TAX

* "...the five considerations for each investment and how the investment fits into your overall investing strategy:

1. Earn/create- how will it generate cash flow for you?

2. Manage- how will you manage this investment?

3. Leverage- how much leverage will the investment provide, or can you get?

4. Protect- how should you hold the investment, maximise its profitability and protect it from potential creditors?

5. Exit- how will you get your original investment money back?"

That last quote from the book is imo, one of the MOST important part of the investing process. Answering those five points prior to investing will mean you've looked at all the aspects of the cash flow, the potential benefits, protecting your asset and finally, being able to extract your capital so that you can invest in additional assets.

Investing for cash flow is a VERY important concept. If you only invest for capital gains and employ negative gearing as your dominant investment strategy, eventually you will hit a debt servicing capacity wall and be unable to service further investment leveraging due to poor cash flow.

It's been a long time since I've written a book review and now I remember why I don't post book reviews often lol. PHEW!! It has been over two years since I've published material regarding personal finance books. The last one I wrote two years ago, 'Top 10 Books on Wealth' is STILL relevant because they're classic books. You should read that post if you like reading personal financial management books.

Thursday, December 6, 2012

Gaining Traction In The Australian PF Blog Market

Due to blog traffic increasing, this has resulted in SMG gaining traction in the personal finance market in Australia. What has been happening?

I've had a few proposals from companies wanting to offer affiliate products and offering to pay commissions via affiliate product sales (so far I'm not interested). Companies wanting to pay me to publish their articles and companies wanting my blog to give them links out using particular anchor text.

I also get plenty of requests wanting free plugs, guest posting etc but so far that doesn't really interest me either.

The latest queries wishing to form some type of relationship has been from Australian based marketing firms on behalf of their clients. I don't know whether I should take the leap and venture deeper into paid territory because that may possibly influence me into publishing something that I may not morally agree with nor believe will be beneficial for readers.

Never thought I'd reach a blogging point where there would be sufficient visits to this blog to garner interest from marketing firms. It's been very interesting...

If I had started a food blog then I would have happily leaped into offers to dine and sample new cuisines without a single thought lol ...but because I write primarily about personal finance and money, I have to be more diligent and careful that I don't mislead you by promoting financial products and or sites that are detrimental to your finances.

I've had a few proposals from companies wanting to offer affiliate products and offering to pay commissions via affiliate product sales (so far I'm not interested). Companies wanting to pay me to publish their articles and companies wanting my blog to give them links out using particular anchor text.

I also get plenty of requests wanting free plugs, guest posting etc but so far that doesn't really interest me either.

The latest queries wishing to form some type of relationship has been from Australian based marketing firms on behalf of their clients. I don't know whether I should take the leap and venture deeper into paid territory because that may possibly influence me into publishing something that I may not morally agree with nor believe will be beneficial for readers.

Never thought I'd reach a blogging point where there would be sufficient visits to this blog to garner interest from marketing firms. It's been very interesting...

If I had started a food blog then I would have happily leaped into offers to dine and sample new cuisines without a single thought lol ...but because I write primarily about personal finance and money, I have to be more diligent and careful that I don't mislead you by promoting financial products and or sites that are detrimental to your finances.

Friday, November 30, 2012

IQ Test Puzzles

In London, there was an awesome Science Museum which sold plenty of puzzles and brain boggling puzzles. I bought an IQ Test from Dynamo House to try because I like those puzzles and think they're fun. They require our minds to think logically but not in a direct line.

If you enjoyed the Legs Puzzle that I posted up a few months ago, you may like to try some of these IQ test puzzles:

Puzzle 1: Mary had a number of cookies. After eating one, she gave half the remainder to her sister. After eating another cookie, she gave half of what was left to her brother. Mary now had only five cookies left. How many cookies did she start with?

11-22-23-45-46 ?

Puzzle 2: A spaceship received three messages in a strange language from a distant planet. The astronauts studied these messages and found that "Elros Aldarion Elendil" means "Danger Rocket Explosion" and "Edain Mnyatur Elros" means "Danger Spaceship Fire" and "Aldarion Gimilzor Gondor" means "Bad Gas Explosion". What does "Elendil" mean?

DANGER-EXPLOSION-NOTHING-ROCKET-GAS?

Puzzle 3: John, twelve years old, is three times as old as his brother. How old will John be when he is twice as old as his brother?

15-16-18-20-21?

Puzzle 4: The price of an article was cut 20% for a sale. By what percent must the item be increased again to sell the article at the original price?

15%-20%-25%-30%-40%?

Enjoy and I'll post up the answers in a few days (or weeks) time =)

If you enjoyed the Legs Puzzle that I posted up a few months ago, you may like to try some of these IQ test puzzles:

Puzzle 1: Mary had a number of cookies. After eating one, she gave half the remainder to her sister. After eating another cookie, she gave half of what was left to her brother. Mary now had only five cookies left. How many cookies did she start with?

11-22-23-45-46 ?

Puzzle 2: A spaceship received three messages in a strange language from a distant planet. The astronauts studied these messages and found that "Elros Aldarion Elendil" means "Danger Rocket Explosion" and "Edain Mnyatur Elros" means "Danger Spaceship Fire" and "Aldarion Gimilzor Gondor" means "Bad Gas Explosion". What does "Elendil" mean?

DANGER-EXPLOSION-NOTHING-ROCKET-GAS?

Puzzle 3: John, twelve years old, is three times as old as his brother. How old will John be when he is twice as old as his brother?

15-16-18-20-21?

Puzzle 4: The price of an article was cut 20% for a sale. By what percent must the item be increased again to sell the article at the original price?

15%-20%-25%-30%-40%?

Enjoy and I'll post up the answers in a few days (or weeks) time =)

Thursday, November 29, 2012

Establishing Goals And Dreams

Yesterday I posted a recap of 2012.

Mr SMG looks up from his iPad in surprise that I finally updated this blog, reads it and then grumbles about how going snowboarding in Canada and Colorado is unfeasible due to our commitments and plans for 2013. It is rather disappointing to know that we may be missing a few snowboarding seasons.

We will be going away to Singapore in a few weeks time, having returned from Europe not long ago. So can't afford to jet off to multiple holidays plus an overseas wedding in addition to buying a freakingly expensive house in Sydney.

I'm rather trepidacious about the potentially monstrous mortgage and have compiled several what-if worse case scenarios if anything goes wrong - what I'll liquidate first (the emergency funds in the mortgage offset), liquidate secondly (my stock portfolio and his managed funds) and liquidate as last resort (my apartment).

I'm being overly dramatic though. We can still afford the potential house mortgage for approximately two years with both of us not earning any direct income from employment before we hit the wall and need to liquidate the illiquid assets such as my apartment. So yeah, haven't bought the house yet but have already crunched the various scenarios into a pile of crumbs already.

So here are my rough goals(again) going forward into 2013, reposted with edits:

1. Something massive x 2 (could I be more 007 like? lol)

2. Buy a house

3. If time+budget+life permits, travel South East Asia (Thailand/Cambodia/Vietnam)

4. Work on side hobbies (photo props/card designs/iPhone apps) and get them launched

Just remembered that I also did a recap of 2011 goals which you can read about here.

Oddly enough, the goals that I hadn't fully achieved in 2011 were all achieved in 2012.

The goals that I haven't fully achieved in 2012 will undoubtedly be achieved in 2013.

Below is a how-to guide on how to set goals and objectives if you don't know how or you wish to learn how. Remember, that all goals must meet the S.M.A.R.T criterias of being specific, measurable, achievable, realistic and timely. You can always sneak in some pie-in-the-sky goals like I always do...you just never know what may come true ;)

Setting Goals And Objectives:

1. What do you want to achieve in the long term 5-10 years from now?

2. What do you want to achieve in the medium term 3-5 years from now to achieve your long term goals?

3. What do you need to do in the short term, today-3 years time to achieve your medium and long term goals?

4. Establish your dreams and goals for various categories such as: family, friends, personal relationship, career, health, finances. For each of those categories, break them down into what you want for the long term and what you need to do in the short to medium term in order to realistically achieve those long term goals.

Note that the time periods are just a guidance and you don't have to set long term, 10 year goals.

However Robert Kiyosaki writes that you need to start off with what and where you want to be in 5-10 years time before you know what you need to do for the next few years to get to where you want to be. (It's blatantly obvious that I've been reading Kiyosaki's books eh?!)

Example Of How To Set Your Goals

A friend of mine tells me that he wants to buy a house. I asked him when does he hope to buy one? He says he doesn't know when and he's got no idea when or how he can afford one. I asked him a few questions to sort out what he wants:

* Which area does he like and wish to buy a house in? Coastal

* What type of house does he want? At least 3 bedrooms, 1 bathroom and 1 carpark

* What are the prices of houses like that in the area he wants to buy in? $500,000

From those answers, we deduced that:

1. He'll need to save up 20% of $500,000 as a deposit

2. He'll need to save up 5% of $500,000 for the miscellaneous expenses such as legal fees, stamp duty, mortgage duty, pest and building inspections, settlement fees etc

3. Therefore he'll need to save up at least $125,000 to buy a house

4. How much can he save each week? $125,000 divided by what he can save weekly or monthly will determine how long it will take him to realistically achieve his long term goal.

Example: If he can save $800 per week, then his goals would look something like:

$125,000/$800 = 156 weeks worth of savings = 3 years worth of saving

1. Long term goal- buy a $500,000 house in 3 years time

2. Medium term - save up at least $41,666 annually

3. Short term - save up $800 per week

So instead of drifting along with the idea that he wants to buy a house in the near future, he can set realistic goals and KNOW that he can buy one in three years time IF he saves $800 weekly.

Mr SMG looks up from his iPad in surprise that I finally updated this blog, reads it and then grumbles about how going snowboarding in Canada and Colorado is unfeasible due to our commitments and plans for 2013. It is rather disappointing to know that we may be missing a few snowboarding seasons.

We will be going away to Singapore in a few weeks time, having returned from Europe not long ago. So can't afford to jet off to multiple holidays plus an overseas wedding in addition to buying a freakingly expensive house in Sydney.

I'm rather trepidacious about the potentially monstrous mortgage and have compiled several what-if worse case scenarios if anything goes wrong - what I'll liquidate first (the emergency funds in the mortgage offset), liquidate secondly (my stock portfolio and his managed funds) and liquidate as last resort (my apartment).

I'm being overly dramatic though. We can still afford the potential house mortgage for approximately two years with both of us not earning any direct income from employment before we hit the wall and need to liquidate the illiquid assets such as my apartment. So yeah, haven't bought the house yet but have already crunched the various scenarios into a pile of crumbs already.

So here are my rough goals(again) going forward into 2013, reposted with edits:

1. Something massive x 2 (could I be more 007 like? lol)

2. Buy a house

3. If time+budget+life permits, travel South East Asia (Thailand/Cambodia/Vietnam)

4. Work on side hobbies (photo props/card designs/iPhone apps) and get them launched

Just remembered that I also did a recap of 2011 goals which you can read about here.

Oddly enough, the goals that I hadn't fully achieved in 2011 were all achieved in 2012.

The goals that I haven't fully achieved in 2012 will undoubtedly be achieved in 2013.

Below is a how-to guide on how to set goals and objectives if you don't know how or you wish to learn how. Remember, that all goals must meet the S.M.A.R.T criterias of being specific, measurable, achievable, realistic and timely. You can always sneak in some pie-in-the-sky goals like I always do...you just never know what may come true ;)

Setting Goals And Objectives:

1. What do you want to achieve in the long term 5-10 years from now?

2. What do you want to achieve in the medium term 3-5 years from now to achieve your long term goals?

3. What do you need to do in the short term, today-3 years time to achieve your medium and long term goals?

4. Establish your dreams and goals for various categories such as: family, friends, personal relationship, career, health, finances. For each of those categories, break them down into what you want for the long term and what you need to do in the short to medium term in order to realistically achieve those long term goals.

Note that the time periods are just a guidance and you don't have to set long term, 10 year goals.

However Robert Kiyosaki writes that you need to start off with what and where you want to be in 5-10 years time before you know what you need to do for the next few years to get to where you want to be. (It's blatantly obvious that I've been reading Kiyosaki's books eh?!)

Example Of How To Set Your Goals

A friend of mine tells me that he wants to buy a house. I asked him when does he hope to buy one? He says he doesn't know when and he's got no idea when or how he can afford one. I asked him a few questions to sort out what he wants:

* Which area does he like and wish to buy a house in? Coastal

* What type of house does he want? At least 3 bedrooms, 1 bathroom and 1 carpark

* What are the prices of houses like that in the area he wants to buy in? $500,000

From those answers, we deduced that:

1. He'll need to save up 20% of $500,000 as a deposit

2. He'll need to save up 5% of $500,000 for the miscellaneous expenses such as legal fees, stamp duty, mortgage duty, pest and building inspections, settlement fees etc

3. Therefore he'll need to save up at least $125,000 to buy a house

4. How much can he save each week? $125,000 divided by what he can save weekly or monthly will determine how long it will take him to realistically achieve his long term goal.

Example: If he can save $800 per week, then his goals would look something like:

$125,000/$800 = 156 weeks worth of savings = 3 years worth of saving

1. Long term goal- buy a $500,000 house in 3 years time

2. Medium term - save up at least $41,666 annually

3. Short term - save up $800 per week

So instead of drifting along with the idea that he wants to buy a house in the near future, he can set realistic goals and KNOW that he can buy one in three years time IF he saves $800 weekly.

Wednesday, November 28, 2012

Birthdays And More Birthdays

Tis' The Season To Be Birthdays

It's been birthday season for the past few months going into Christmas.

Haven't even had time to contemplate the Silly Season because of Birthday Season.

What have you been up to? Christmas shopping? Just to let you know in advance, this post has a little bit of everything to compensate for the weeks I haven't been prolifically blogging.

The Aussie Economy

Our Aussie economy is in a slump right now and it would be foolish of me to ignore the potentially darker economy heading our way. Maybe we're in a slump because we mutilate ourselves, economically speaking. We buy goods online from overseas and that means local retailers(one of the biggest employers in Oz) are struggling and this translates to cut labour hours and reduced income for retail employees. All this flow on effect leads to reduced consumption. It's the circle of economics 101.

Travelling and More Travelling

Mr SMG and I will be travelling again in a few short weeks to Singapore. We're actually driving south with a group of friends next weekend. So much happening. There was a looooong hiatus from blogging because we were in Europe for several weeks. I can't even disclose exactly when we'll be travelling because there are other third parties out there who know where I live. That's what happens when you post under your real name duh, *smacks forehead*.

I had good intentions of posting up some holiday snaps but it's been crazy busy even though I supposedly have almost all the time in the world. Over the last few months, I've been thanking my younger, sagacious self for looking after my older self. I could not be in my current position of relative comfort without my younger self prudently investing madly(juxtaposition intended lol).

Coulda, Woulda, Shoulda

Yours truly has been preoccupied with an iPhone app idea. Will that venture take off or crash and burn?

I won't even shed any tears over how my dear friend Mr Z and I could have been gazillionaires already if we had bought Apple shares back in 2006/2007. He and I could have had ten million each under our belts if we had chosen that route but when the road is forking, you never know which road to take until it's too late. Who could have foreseen the successful, phenomenal Apple product releases of the iPad and iPhones? We knew Apple's imagination and creativity was starting to ignite back then, but as you know, coulda, woulda, shoulda. Oops.

An Early Christmas Pressie For You

What can I give my readers for Christmas? Maybe a wry comment to go easy on the credit card and Christmas gifts if you think you may end up with a financial headache in January. Go through your recurring bills and find more competitive offers out there, ask for a price match and save yourselves thousands of dollars. What else hasn't been said?

New Years Eve Resolution For 2013

Okay, so I'm one month early =) Why wait?

If you've got NYE resolution from back in January, maybe reflect on those and what you've achieved?

I look back at what I posted in January 2012 about my NYE resolutions:

2. Nope; didn't buy the house

3. Yep; few travel destinations were travelled

Two out of three ain't bad I guess. It would have been sweet to achieve all three but I'm still happy overall about 2012 =)

Got some MAJOR plans for 2013:

1. Something massive x 2 (could I be more 007 like? lol)

2. Buy a house

3. If time+budget+life permits, go snowboarding in Canada/Colorado

(Mr SMG says this is pie in the sky and I should have omitted this one >.<)

4. If time+budget+life permits, travel South East Asia (Thailand/Cambodia/Vietnam)

5. Work on side hobbies (photo props/card designs/iPhone apps) and get them launched

What about yourself? Are you happy with 2012?

It's been birthday season for the past few months going into Christmas.

Haven't even had time to contemplate the Silly Season because of Birthday Season.

What have you been up to? Christmas shopping? Just to let you know in advance, this post has a little bit of everything to compensate for the weeks I haven't been prolifically blogging.

The Aussie Economy

Our Aussie economy is in a slump right now and it would be foolish of me to ignore the potentially darker economy heading our way. Maybe we're in a slump because we mutilate ourselves, economically speaking. We buy goods online from overseas and that means local retailers(one of the biggest employers in Oz) are struggling and this translates to cut labour hours and reduced income for retail employees. All this flow on effect leads to reduced consumption. It's the circle of economics 101.

Travelling and More Travelling

Mr SMG and I will be travelling again in a few short weeks to Singapore. We're actually driving south with a group of friends next weekend. So much happening. There was a looooong hiatus from blogging because we were in Europe for several weeks. I can't even disclose exactly when we'll be travelling because there are other third parties out there who know where I live. That's what happens when you post under your real name duh, *smacks forehead*.

I had good intentions of posting up some holiday snaps but it's been crazy busy even though I supposedly have almost all the time in the world. Over the last few months, I've been thanking my younger, sagacious self for looking after my older self. I could not be in my current position of relative comfort without my younger self prudently investing madly(juxtaposition intended lol).

Coulda, Woulda, Shoulda

Yours truly has been preoccupied with an iPhone app idea. Will that venture take off or crash and burn?

I won't even shed any tears over how my dear friend Mr Z and I could have been gazillionaires already if we had bought Apple shares back in 2006/2007. He and I could have had ten million each under our belts if we had chosen that route but when the road is forking, you never know which road to take until it's too late. Who could have foreseen the successful, phenomenal Apple product releases of the iPad and iPhones? We knew Apple's imagination and creativity was starting to ignite back then, but as you know, coulda, woulda, shoulda. Oops.

An Early Christmas Pressie For You

What can I give my readers for Christmas? Maybe a wry comment to go easy on the credit card and Christmas gifts if you think you may end up with a financial headache in January. Go through your recurring bills and find more competitive offers out there, ask for a price match and save yourselves thousands of dollars. What else hasn't been said?

New Years Eve Resolution For 2013

Okay, so I'm one month early =) Why wait?

If you've got NYE resolution from back in January, maybe reflect on those and what you've achieved?

I look back at what I posted in January 2012 about my NYE resolutions:

"a huge promise to make, a house to buy and a few travel destinations"1. Yep; the huge promise was made

2. Nope; didn't buy the house

3. Yep; few travel destinations were travelled

Two out of three ain't bad I guess. It would have been sweet to achieve all three but I'm still happy overall about 2012 =)

Got some MAJOR plans for 2013:

1. Something massive x 2 (could I be more 007 like? lol)

2. Buy a house

(Mr SMG says this is pie in the sky and I should have omitted this one >.<)

4. If time+budget+life permits, travel South East Asia (Thailand/Cambodia/Vietnam)

5. Work on side hobbies (photo props/card designs/iPhone apps) and get them launched

What about yourself? Are you happy with 2012?

Friday, November 9, 2012

Traffic Stats: Over 100,000 visits to SMG

Sorry dear readers. Haven't been posting consistently. Just wanted to say that I thank you for visiting, for reading and for subscribing.

Just thought I'd do a quick post to say that my Google Analytic traffic stat has hit over 100,000 visits to this humble site. It may not be a super huge number but it means that I'm writing something that is of interest or of use to you as readers.

Even without posting regularly, the views last month was crazy at 15, 696. The figures are growing exponentially.

My 'statcounter' is only tracking visits to the main homepage(almost 47,000), whereas Google Analytics track visits to all parts of my blog, including archives.

Just thought I'd do a quick post to say that my Google Analytic traffic stat has hit over 100,000 visits to this humble site. It may not be a super huge number but it means that I'm writing something that is of interest or of use to you as readers.

Even without posting regularly, the views last month was crazy at 15, 696. The figures are growing exponentially.

My 'statcounter' is only tracking visits to the main homepage(almost 47,000), whereas Google Analytics track visits to all parts of my blog, including archives.

Wednesday, November 7, 2012

Harvesting, Pruning and Eating Your Basil Plants

A friend of ours was showing me his super healthy, potted herb garden.

I envy folks who live in houses. House gardens are much more conducive to gardening than most balcony gardens. Our balcony gets windy most days because of the height and proximity to the river so we get a lot of wind which causes the soil to dry out and harden.

Anyway, for anyone curious about how they can prune or harvest their basil to eat, I'm posting some pictures below of how we harvest ours. All varieties of basil, mint and rosemary thrives on being cut back so that their side buds can grow bushy. Pruning them to eat also prevents them from flowering so that you can enjoy eating them for several months.

It's tempting to let your beloved plants to grow unchecked and uneaten but before you know it, they'll start flowering and it's all over unless you cut all the blooms off before they start seeding and dying off. As you can see below, it doesn't matter where I cut, as long as I remove the flower and cut just above the leaves/shoot nodes:

Cutting your basil or mint plants (it doesn't matter which variety you grow):

1. Decide how high you want your basil plant to grow and aim to lop off at the height you desire

2. Identify the two big fat leaves at the node and the little baby shoots growing from the stem

3. Cut just above the two big fat leaves and the baby shoots and lop the top off

4. Eat

As you can see, our dear friend Peanut, gave us this Thai basil plant months ago. It was too hard to eat Thai basil all the time so it ultimately started flowering because I wasn't pruning them back diligently. I've been stir frying, having basil in the soup, basil in rice paper summer rolls and have been taking a break from basil so they started flowering.

I envy folks who live in houses. House gardens are much more conducive to gardening than most balcony gardens. Our balcony gets windy most days because of the height and proximity to the river so we get a lot of wind which causes the soil to dry out and harden.

Anyway, for anyone curious about how they can prune or harvest their basil to eat, I'm posting some pictures below of how we harvest ours. All varieties of basil, mint and rosemary thrives on being cut back so that their side buds can grow bushy. Pruning them to eat also prevents them from flowering so that you can enjoy eating them for several months.

It's tempting to let your beloved plants to grow unchecked and uneaten but before you know it, they'll start flowering and it's all over unless you cut all the blooms off before they start seeding and dying off. As you can see below, it doesn't matter where I cut, as long as I remove the flower and cut just above the leaves/shoot nodes:

1. Decide how high you want your basil plant to grow and aim to lop off at the height you desire

2. Identify the two big fat leaves at the node and the little baby shoots growing from the stem

3. Cut just above the two big fat leaves and the baby shoots and lop the top off

4. Eat

As you can see, our dear friend Peanut, gave us this Thai basil plant months ago. It was too hard to eat Thai basil all the time so it ultimately started flowering because I wasn't pruning them back diligently. I've been stir frying, having basil in the soup, basil in rice paper summer rolls and have been taking a break from basil so they started flowering.

Thursday, October 18, 2012

Henderson Poverty Index And Household Expenditure Measure

Have you heard of the HPI (Henderson Poverty Index) or HEM (Household Expenditure Measure)?

HPI and HEM are the living expense amounts that lenders use in their mortgage calculators to see how much you can borrow.

Some home loan lenders have started using the HEM to calculate the maximum size loan you can borrow based on your income. Using HEM in calculations means individuals can borrow more while it's the inverse for couples, that is couples can borrow less when the HEM is used.

When you apply for a mortgage loan, the paperwork will ask you to state your living expenses and how much you spend. With those figures, they will compare it to the appropriate category in the tables below and take the higher figure to use in their mortgage calculators.

If you're single, is $1105 per month sufficient to meet your living expenses?

If you're a couple, is $2032 per month sufficient to meet your living expenses?

Source:

1. homeloanexperts.com.au

HPI and HEM are the living expense amounts that lenders use in their mortgage calculators to see how much you can borrow.

Some home loan lenders have started using the HEM to calculate the maximum size loan you can borrow based on your income. Using HEM in calculations means individuals can borrow more while it's the inverse for couples, that is couples can borrow less when the HEM is used.

When you apply for a mortgage loan, the paperwork will ask you to state your living expenses and how much you spend. With those figures, they will compare it to the appropriate category in the tables below and take the higher figure to use in their mortgage calculators.

Living expenses for single adults

| Household Segments | HPI | HEM |

| No Dependents | $1250 | $1105 |

| 1 Dependent | $1717 | $1430 |

| 2 Dependents | $2159 | $1560 |

| 3 Dependents | $2601 | $1889 |

Living expenses for couples

| Household Segments | HPI | HEM |

| No Dependent | $1817 | $2032 |

| 1 Dependent | $2284 | $2583 |

| 2 Dependents | $2726 | $2704 |

| 3 Dependents | $3168 | $3137 |

If you're single, is $1105 per month sufficient to meet your living expenses?

If you're a couple, is $2032 per month sufficient to meet your living expenses?

Source:

1. homeloanexperts.com.au

Wednesday, October 17, 2012

Sharing Is Caring: Co-op Websites

Sharing Is Caring

As more and more apartments are built, the traditional concept of houses and neighbourhoods no longer apply.

Apartment dwellers can be faceless and quiet. Sometimes you might bump into a familiar face sharing the lift with you. Some are friendly while some prefer to keep to themselves. Is this a vision of the future or will the sharers and community sort start fighting back to bring community back into our lives?

Children use to play out on the streets together. Neighbours would swap recipes and borrow items that they needed. Nowadays, with the fear about children being kidnapped or injured, the helicopter parents who hover over their kids, the bustling lives that we lead, the long hours that folks work and all the technological gadgets that keep us voluntarily addicted indoors, we no longer socialise as much with our neighbours.

If you ran out of sugar, which one of you readers would feel comfortable enough to knock on your neighbours door and borrow sugar? If you were going away on holiday, would you be comfortable enough to give your house keys to your neighbour to help with tasks such as feeding the dog and watering the plants? If you have a child, do you feel confortable enough to ask them to mind your child for 30 minutes while you pick up something from the local shops?

It's no wonder that social sharing through swapping and community gardens are making such a comeback. There are folks out there who wish to engage in sharing, renting, borrowing, bartering and giving their stuff away for free. They wish to reconnect with their local neighbourhood, to help and be helped in return should they ever need help.

Sharing Can Be Financially and Environmentally Smart

By sharing or giving away items that you no longer need you can reduce land fill. Sharing items you don't use frequently or simply trading your skills for someone else's skills are ways that you can be environmentally friendly whilst also saving you some money.

Sites Where You Can Share

As more and more apartments are built, the traditional concept of houses and neighbourhoods no longer apply.

Apartment dwellers can be faceless and quiet. Sometimes you might bump into a familiar face sharing the lift with you. Some are friendly while some prefer to keep to themselves. Is this a vision of the future or will the sharers and community sort start fighting back to bring community back into our lives?

Children use to play out on the streets together. Neighbours would swap recipes and borrow items that they needed. Nowadays, with the fear about children being kidnapped or injured, the helicopter parents who hover over their kids, the bustling lives that we lead, the long hours that folks work and all the technological gadgets that keep us voluntarily addicted indoors, we no longer socialise as much with our neighbours.

If you ran out of sugar, which one of you readers would feel comfortable enough to knock on your neighbours door and borrow sugar? If you were going away on holiday, would you be comfortable enough to give your house keys to your neighbour to help with tasks such as feeding the dog and watering the plants? If you have a child, do you feel confortable enough to ask them to mind your child for 30 minutes while you pick up something from the local shops?

It's no wonder that social sharing through swapping and community gardens are making such a comeback. There are folks out there who wish to engage in sharing, renting, borrowing, bartering and giving their stuff away for free. They wish to reconnect with their local neighbourhood, to help and be helped in return should they ever need help.

Sharing Can Be Financially and Environmentally Smart

By sharing or giving away items that you no longer need you can reduce land fill. Sharing items you don't use frequently or simply trading your skills for someone else's skills are ways that you can be environmentally friendly whilst also saving you some money.

Sites Where You Can Share

- Neighbourhood sharing: thesharehood.org

- Sharing work spaces: the-hub.net

- Travelling: airbnb.com

- House swaps: houseswap.com

- Social lending to peer groups: lendinghub.com.au

- Trading sites where you can buy or get stuff for free: Ebay.com or gumtree.com.au

Monday, October 15, 2012

Fashion Entrepreneur: Net-a-Porter Natalie Massenet

If you've never heard of Massenet, then you may have heard of the luxury fashion site Net-a-Porter that was sold in 2010 for 350 million pounds, netting Massenet 50 million pounds for her share. Massenet is the founder of the elite fashion shopping site.

Daughter of a US journalist and English model, wife of an investment banker and just 34 years old when she leapt into the world of online retailing back in the early dotcom days of 2000. Graduate of U.C.L.A and former fashion editor.

Net-a-Porter has been designed as such that the value of sales and the location can be viewed immediately by staff. Online shopping sales spikes on rainy days, during lunch times, after 9pm and on Mondays, Wednesdays and Fridays because new stocks are released on those three days. During the early years of operations, she talks of "desperate hand wringing, tears and pleading with brands".

Massenet says, "You'd go all the way through a pitch and say: 'And then you can click and buy it from pictures and it's delivered anywhere in the world.' And they'd listen and they'd nod and then afterwards they'd say: 'Just tell me one more thing: where is your store?' "

Massenet is a proponent of positive thoughts and how it can influence your life, "the power of your thoughts can influence how events turn out. I’m a positive person—when bad things happen, I can see the silver lining. As a result I think I’m very lucky, even though I probably have as much bad luck as anyone else, and that translates into seeing opportunity."

Unlike other businesses that struggled through the financial crisis starting in 2008, Net-a-Porter experienced meteoric growth. From 2008, they increased their staff head count from 600 to 2000 and turnover increased by over 60%.

Despite the troubles that Massenet encountered in the beginning, together with her partner Quinn, they believed in their idea and their concepts. What they have now with Net-a-Porter is a leading, luxury shopping portel with editorials from famous names in the publishing field such as Lucy Yeoman, previously editor of Harpers Bazaar.

Sources:

1. SMH Money

2. fashion.telegraph.co.uk

3. http://www.smartcompany.com.au

Thursday, October 11, 2012

Importance Of Sleeping

There's so much to do, watch, see and read and not enough time in the day right?

You may have heard about how important sleep is right? Every now and again, I struggle to fall asleep so sleeping tips are really useful.

Rapid eye movement, commonly abbreviated to REM, is deepest during the first four hours of sleep. REM and dreaming are very important because it assists in developing memory consolidation. A person sleeping for 8 hours has more REM than one who sleeps for only 5 hours.

However, we can 'survive' on 90 minutes sleep because that is one full sleep cycle. If you can sleep for up to eight hours each night then you can get the benefits of five sleeping cycles.

There are three main categories of insomnia.

1. Transient insomnia- ranges from a few days to a few weeks. Triggered by environmental factors such as noise and temperature

2. Acute insomnia- ranges to a few weeks and can be triggered by anxiety, worries and stress

3. Chronic insomnia-lasting a few years and is dangerous because it impacts on health, safety and quality of life

According to the Women's Health magazine study on sleep, 25% of us sleep for only six hours or less each night. In 2009, one of their surveys found that 44% of Australians had insomnia in the six months period leading up to the survey.

There have been plenty of studies done on sleeping patterns and its effect on us and on lab animals. The University of Chicago conducted a study that involved keeping rats awake. It took two weeks for all of them to die. (Why are we still being cruel to animals for something like this?!).

There was a 17 year old boy in the US who stayed awake for just over 18 days and by then he was suffering a range of symptoms such as "hallucinations, paranoia, blurred vision, slurred speech, memory and concentration lapses."#

Other health issues resulting from poor sleep or lack of sleep are diabetes, heart disease, high blood pressure, irregular heartbeats, inflammation issues (arthritis and bowel disesaes), anxiety, obesity, mental illnesses and depression.

If you're having difficulties getting to sleep, there are some useful techniques that can be utilised:

* Wake up at the same time in the morning so that your body will be eager to tell you to go to bed at night

* If you're having trouble falling asleep, don't lie in bed, get up and read or do something that doesn't involve watching TV and you will get sleepy again

* Try not to use sleeping pills because they reduce your confidence in your natural ability to fall asleep

* Sleep when you're tired and don't wait until you're finished doing whatever it is you wanted to do

* No TV, mobile phones or computers at least for one hour before bedtime, they both expose our brains to 'blue light' which suppresses the release of melatonin, the hormone which tells our body when to sleep

* You would rather be a little cool than too hot